When starting a business, one of the very first decisions you need to make is which type of business entity to form. Since US states create business entities and make the laws regarding which types are available and how they are set up and regulated there is a bit of variety among the states, and therefore there are many varieties available. However, all states offer these entities: business corporations and limited liability companies (LLCs). Business corporations come in two types: C corporations and S corporations, but this is a difference in federal tax status, not an entity-level difference. Each entity type has its own advantages and disadvantages, especially when it comes to taxation. In this article, we will compare S corporations, C corporations, and LLCs from a tax perspective, to help you determine which entity type is right for your business.

Business Entity Comparison

Important things to know

Important things to know

- The “tax statuses” are defined by federal law but corporations and LLCs are formed by state governments, each of whom have their own laws and regulations.

- Changing tax status is a one-time thing to do. It is very expensive to reverse a change.

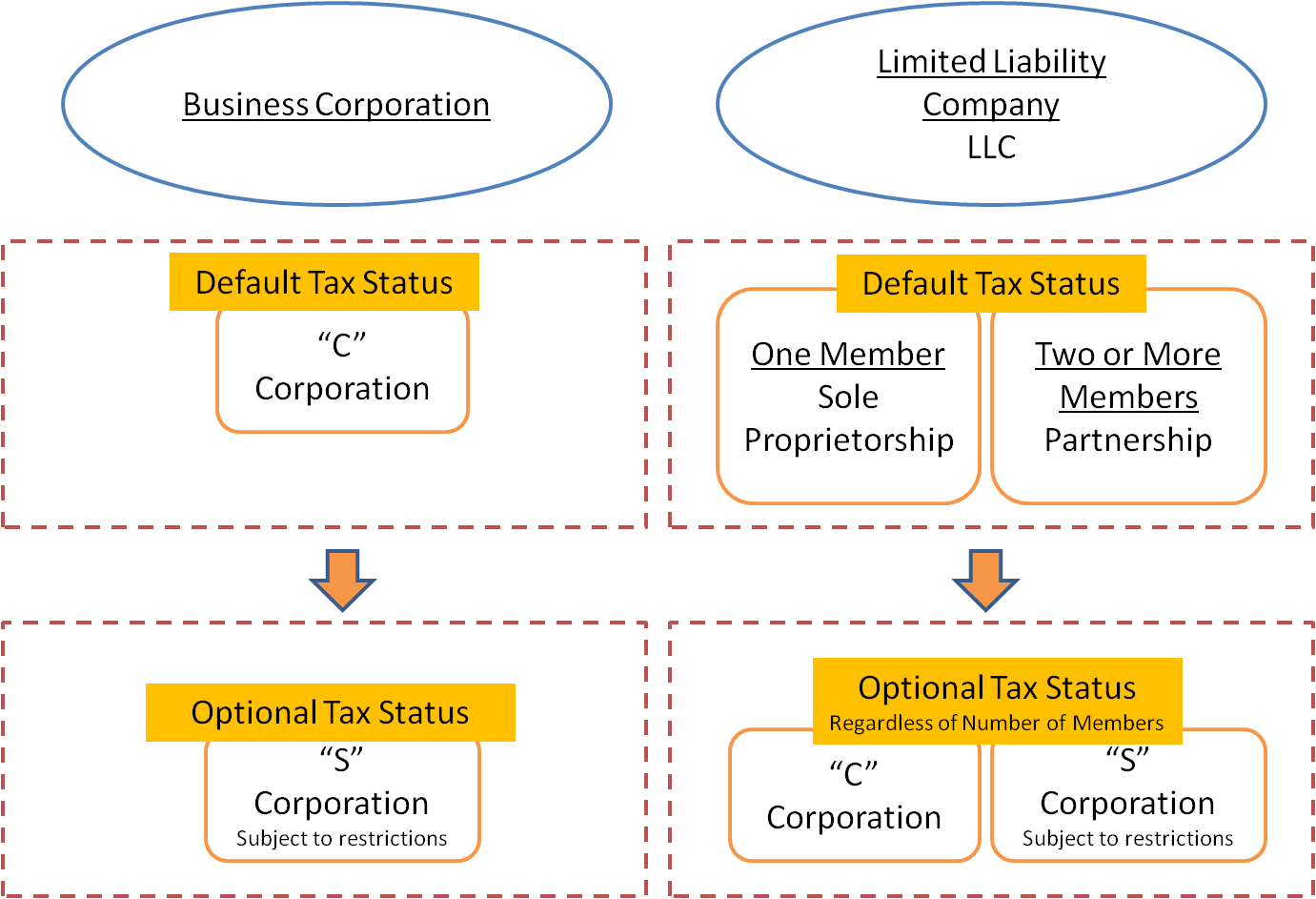

Tax Statuses and Formation

It’s important to note that the tax statuses of S corporations, C corporations, and LLCs are defined by federal law, while these entities are formed by state governments that have their own laws and regulations. The formation process for a C corporation is straightforward, and it is the default status for all corporations. In contrast, LLCs have greater flexibility in their formation, and they can be taxed as either a sole proprietorship, partnership, S corporation, or C corporation.

S Corporation Tax Status

If a corporation meets certain criteria, such as having 100 or fewer shareholders who are individuals or estates, ALL of whom are U.S. citizens or residents, it can choose to become an S corporation. S corporations are often favored by small business owners because they offer tax benefits, such as avoiding the double-taxation of the C corporation. Instead, the company’s profits and losses are passed through to the shareholders’ personal tax returns.

However, there are some drawbacks to consider. For instance, S corporations cannot be a subsidiary of another company, cannot have any non-US resident shareholders and they can only have one class of shares. Additionally, many states require a separate filing to get S status in that state, and changing tax status is a one-time thing to do. It is very expensive to reverse a change.

C Corporation Tax Status

As mentioned earlier, all corporations are created as C corporations by default. C corporations are taxed separately from their shareholders, and they offer more flexibility in terms of ownership and structure. C corporations can issue multiple classes of stock, can have non-US resident shareholders and they can have an unlimited number of shareholders. Because they allow for the creation of preferred shares, startups with (or seeking) venture capital are nearly always going to be C corporations. Profits of a C corporation can be retained in the corporation indefinitely, subject to excessive retained earnings limitations, thus building up the capital of the corporation.

However, C corporations are subject to double taxation, which means the corporation pays taxes on its profits, and then shareholders pay taxes again on any dividends they receive. Additionally, some deductions available to C corporations are not available to S corporations, such as fringe benefits.

LLC Tax Status

LLCs offer the most flexibility in terms of ownership and structure. By default, they are considered “pass-through” entities, which means that the company’s profits and losses are passed through to the owners’ personal tax returns, similar to an S corporation. LLCs can be taxed as a sole proprietorship, partnership, S corporation, or C corporation, depending on the number of members and what election has been made, if any.

However, LLCs have some drawbacks to consider as well. For instance, they offer fewer tax benefits than S corporations, and they are subject to self-employment taxes. Additionally, while LLCs have greater flexibility in terms of ownership and management, they may also have more complex governance requirements.

Conclusion

In summary, S corporations, C corporations, and LLCs all have their own advantages and disadvantages from a tax perspective. Choosing the right entity type for your business will depend on a variety of factors, such as your business goals, ownership structure, and tax situation. It’s important to consult with a tax professional or business attorney before making any decisions. Learn more about tax statuses at the IRS website for the federal tax perspective.